[ad_1]

- Practically 130 nations final week agreed to “halt and reverse forest loss and land degradation” by 2030. Accompanying that declaration was a dedication to allocate $19.2 billion towards that purpose. However how will these sources be deployed within the Amazon?

- A few of that cash is predicted to go towards reforming the manufacturing programs that drive deforestation. That cash would probably matched by even bigger quantities of personal capital searching for so-called “inexperienced investments.” How that cash is channeled and who advantages will decide whether or not Amazonian societies tackle the long-standing social inequality that can be a key driver of deforestation.

- In “A Excellent Storm within the Amazon Wilderness”, Tim Killeen gives an outline of rural finance with a particular deal with mechanisms designed to assist smallholders. Killeen additionally takes a important take a look at the rising marketplace for “inexperienced bonds”

- This publish is an besides from a guide. The views expressed are these of the writer, not essentially Mongabay.

Editor’s word: Tim Killeen gives an replace on the state of the Amazon in his new guide “A Excellent Storm within the Amazon Wilderness – Success and Failure within the Battle to avoid wasting an Ecosystem of Essential Significance to the Planet.”

The guide gives an outline of the subjects most related to the conservation of the Amazon’s biodiversity, ecosystem providers and Indigenous cultures, in addition to an outline of the standard and sustainable improvement fashions vying for area throughout the regional economic system.

The narrative explains the social and financial realities that constrain the selections of stakeholder teams and financial actors and motivates them to behave as they do. It additionally identifies the insurance policies which have created a basis for change within the area, in addition to these that aren’t delivering the advantages their advocates had hoped to generate.

Mongabay will publish excerpts from the Killeen’s guide, which might be launched by The White Horse Press in serial format over the course of the subsequent yr (Killeen can be working to adapt the guide into Spanish and Portuguese). On this third installment, we offer a piece from Chapter three: Agriculture: Profitability determines land use. You may learn the primary at The political economic system of the Pan-Amazon and second at New transport infrastructure is opening the Amazon to international commerce. Killeen has a GoFundMe marketing campaign right here.

Practically 130 nations final week agreed to “halt and reverse forest loss and land degradation” by 2030. Accompanying that declaration was a dedication to allocate $19.2 billion towards that purpose. However how will these sources be deployed within the Amazon?

If the messaging within the declaration is to believed, a portion of that cash will go towards Indigenous peoples’ and native communities’ efforts to steward their lands. However a few of that cash is predicted to go towards reforming the manufacturing programs that drive deforestation. That cash would probably matched by even bigger quantities of personal capital searching for so-called “inexperienced investments.” How that cash is channeled and who advantages will decide whether or not Amazonian societies tackle the long-standing social inequality that can be a key driver of deforestation.

Each nation within the Pan Amazon has a system for channeling monetary sources to producers within the rural economic system, with totally different mechanisms for companies, communities and households. Some are properly designed. Some not a lot. Coverage makers want to know what exists earlier than they begin throwing cash at complicated programs characterised by inequality and a deeply ingrained aversion to danger.

Rural finance within the Amazon

The agricultural producers of the Amazon have entry to radically totally different ranges of credit score relying upon nationwide insurance policies, the willingness of every nation’s monetary providers business to interact rural populations and, most significantly, the size of their manufacturing system. Brazil has essentially the most refined agricultural sector and, not surprisingly, essentially the most beneficiant and far-reaching system to assist its producers. Industrial-scale farmers have entry to a number of types of credit score, which they entry to pay operational prices, purchase expertise and put money into on-farm infrastructure. If they’re entrepreneurial, and lots of are, they borrow cash to accumulate land and develop manufacturing. Small household farms have fewer choices, however the federal authorities has applications to offer them with inexpensive short-term credit score. Regardless, the money economic system predominates on forest frontiers and inside smallholder landscapes the place producers should overcome obstacles imposed by bodily isolation and subsistence livelihoods. Monetary credit score to assist manufacturing is basically absent within the Andean Amazon, the place small farmers function inside an off-the-cuff economic system with restricted entry to monetary providers.

Brazil’s monetary system operates on two tracks: the Sistema Nacional de Crédito Rural (SNCR), which is managed by the monetary business in accordance with guidelines established by the federal authorities; and an unbiased system managed by multinational buying and selling corporations designed to seize commodities for his or her competing provide chains. The latter consists of the 4 well-known western giants: ADM, Cargill, Bunge and Louis Dreyfus, in addition to second-tier corporations based mostly in Brazil (Amaggi), Japan (Gavilon), Europe (Sodrugestvo) and China (COFCO). Inside the Amazon, the SNCR gives many of the credit score utilized by the livestock sector, whereas the area’s grain farmers rely upon credit score obtained from the SNCR, loans from business banks and, most significantly, short-term credit score offered by commodity merchants.

The SNCR was established in 1965 along side authorities insurance policies to advertise settlement and funding within the agricultural frontiers of the Southern Amazon. Its fundamental goal is to offer producers with working capital at below-market rates of interest to allow them to plant and harvest a crop or elevate a herd of cattle for slaughter. The nationwide rural finance plan (Plano Safra) of 2020/2021 offered $R 236 billion (~$45 billion) in loans to the livestock, farm and plantation sectors; 75% was used for short-term credit score, and 25% was allotted for medium to long-term investments. Small producers had entry to R$ 33 billion with curiosity between 2.75% and 4%, whereas medium-sized producers obtained an identical sum at 5%. Giant-scale producers, who obtain the majority of the finance, had been charged between 6 and seven% annual curiosity. [i]

The SNCR program has been, and stays, an necessary aspect in nationwide improvement methods and has catalyzed the spectacular development of Brazilian agriculture. The success of the SNCR rests on its means to leverage the home financial savings of the Brazilian individuals with the technical capability of Brazil’s business banking sector. Its genius was to offer low-cost credit score to strategically necessary producers in an economic system characterised by excessive rates of interest. The lion’s share of the SNCR’s monetary sources is generated by a regulatory requirement that obligates business and financial savings banks to both: (a) switch 34 per cent of their deposits to the Banco Central do Brasil or (b) use these sources to fund mortgage portfolios in agriculture and forestry. [ii] Enticing rates of interest are a magnet for buyers, particularly when mixed with an simply understood enterprise mannequin based mostly on standard economics. Brazil’s plentiful soil and water sources are the inspiration of its rural economic system, however the SNCR shares a lot of the credit score for creating an agricultural powerhouse. It additionally shares accountability for the conversion of roughly eighty million hectares of Amazonian rainforest and an roughly equal space of Cerrado savannas. [iii]

The SNCR channeled lots of of tens of millions of {dollars} into the Southern Amazon in the course of the Nineteen Seventies to ascertain a cattle business on land being distributed to influential households and firms. [iv] Within the Nineteen Eighties, this system loaned cash throughout a interval of hyperinflation at rates of interest properly under the speed of inflation, an untenable scenario that led to its near-collapse within the early Nineteen Nineties. The SNCR was revitalized following the stabilization of the Brazilian economic system within the administration Fernando Henrique Cardoso, who launched two extra applications managed by the nationwide improvement financial institution: PRONAF, which is focused at smallholders, and PRONAMP, which gives finance to medium-scale producers. Regional improvement banks, generally known as Fundos Constitucionais de Financiamento, even have credit score applications focused at their rural constituents. [v]

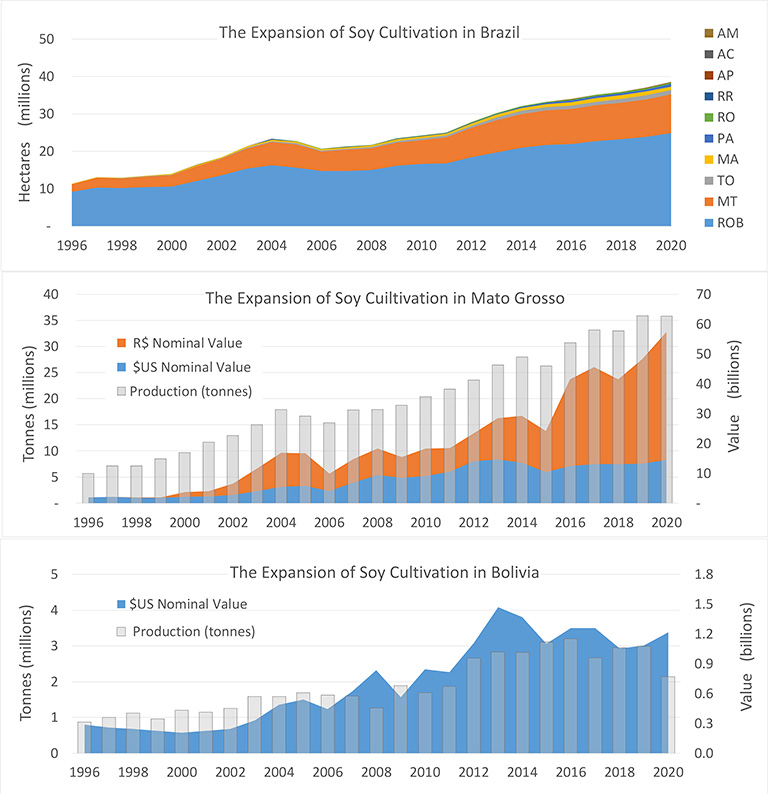

A current evaluate revealed that between $9 and 12 billion {dollars} had been loaned yearly by way of the SNCR to Amazonian producers over the past decade. Of this quantity, roughly 44% went to Mato Grosso, adopted by Tocantins (18%), Pará (13%), Maranhão (13%), and Rondônia (9%). [vi] This examine appeared solely at 4 commodities thought of to be the primary drivers of deforestation and reported that 64% of the loans went to cattle ranchers and 35% to soy farmers, with smaller quantities to timber (0.5%) and oil palm plantations (0.7%). Information for PRONAF had been reported solely on the nationwide degree, however small farmers cultivating soy, beef and palm oil obtained solely two p.c of the sources channeled by way of the SNCR.

The contribution of the buying and selling corporations is tough to know as a result of they don’t escape these numbers of their annual reviews. They are often estimated, nonetheless, utilizing bottom-up strategies and authorities reported statistics. Within the 2019/2020 crop-year, soy and maize had been cultivated on roughly eighteen million hectares within the states of the Authorized Amazon, the place the main extension company reported the price of seed, gas, agrochemicals and labour at $650 per hectare. [vii] Assuming {that a} hundred per cent of crop is planted and harvested utilizing short-term credit score, then agribusiness would want roughly $13 billion to plant and harvest a crop. Since solely $1.6 billion was obtained by way of the SNCR, [viii] the remaining $11.4 billion was most likely provided by the commodity buying and selling corporations. That could be an overestimate, nonetheless, as a result of large-scale producers, who management roughly 46 per cent of the agricultural land in Brazil, are sometimes subsidiaries of diversified firms. As such, they’ve entry to a number of types of credit score, together with home bond markets and abroad non-public fairness. [ix]

Bond markets embody company bonds, that are ‘debentures’ backed by the popularity of the corporate and Certificados de Recebíveis do Agronegócio (CRA); these are securities that place a lien on a bodily or contractual asset. Each are utilized by agribusinesses and banks to finance medium to long-term investments (two to 12 years). If the CRA is issued by a financial institution, it’s prone to be a basket of loans to household farmers, whereas firms use them to fund particular person tasks or actions. The Brazilian bond market has attracted worldwide consideration over the past a number of years (post-2015) as a result of it’s considered as a venue for sustainable finance that seeks to minimise danger from ‘environmental, social and governance’ (ESG) components that hurt society and, presumably, enhance the chance of shedding cash.

The commonest sorts, and the most important by quantity ($10 billion) have been ‘inexperienced bonds’ issued by firms accessing capital markets with out the intermediation of banks. Within the Amazon, corporations are committing to devour (self-generated) renewable vitality, enhance productiveness, sequester soil carbon and, allegedly, preserve biodiversity and water sources. One of many largest initiatives is FS Bioenergia ($639 million) a maize-based ethanol producer that could be a three way partnership between the Iowa-based Summit Holdings and a Tapajos Participaes S/A, a Brazilian subsidiary of a Chinese language holding firm (Hunan Dakang). Brazilian agribusiness giants are likewise accessing the inexperienced bond market, together with SLC Agrícola ($480 million) that farms 150,000 hectares in Mato Grosso and Maranhão; and Amaggi S/A ($750 million), which operates an built-in provide chain spanning 259,000 hectares in Mato Grosso and consists of logistics and processing services in Rondônia, Amazonas and Pará. [x]

One of the vital controversial choices, is a ‘transitional mortgage’ to Marfrig Alimentos S/A ($430 billion), a beef packing firm dedicated to eliminating unlawful deforestation and unfair labour practices from its provide chain. The tender is classed as a mortgage quite than a bond because of the contractual phrases of the providing; it’s controversial as a result of many of the sources might be used to assist their devoted provide chain (Marfrig Membership) with out sufficient ensures to reform or exclude calves originating from unbiased producers who aren’t in compliance with the Forest Code. [xi] The factors for evaluating the ESG efficiency will depend on Key Efficiency Indicators (KPIs) specified within the prospectus of particular person which are validated by unbiased third occasion evaluate.

There may be solely restricted potential for finance to vary agricultural practices within the Andean Amazon, as a result of landscapes are largely populated by smallholders who’re notoriously risk-adverse in how they handle their funds and cropping programs. They’re cautious as a result of the results of a crop failure are catastrophic for his or her households; consequently, they’re much less prone to undertake novel manufacturing programs that require a capital funding that must be financed by debt. Practically all perceive the worth of credit score and its potential to rework their lives; nonetheless, the choices out there to them are neither pleasant nor honest. [xii]

Andean governments have launched a number of efforts over a number of many years attempting to create mechanisms and establishments to offer monetary credit score for rural communities, however they’ve failed to vary the calculus that impedes funding on smallholder landscapes. One manifestation of the problem is the excessive proportion of households which are unbanked, a time period economists use to explain people who, by alternative or circumstance, don’t use monetary providers. One other is the function of microfinance establishments that present credit score to people who don’t qualify for loans from standard banks; as an alternative, they borrow cash based mostly on ‘good religion’ and reputational integrity. Their presence has materially benefitted the lives of tens of 1000’s of people, lots of them girls, by permitting them to take part within the casual market economic system that characterizes commerce in these nations. As well as, they provide financial savings accounts and supply households with a digital id for interacting with authorities businesses and utility corporations. Sadly, these establishments lend cash at rates of interest which are out of attain for small farmers.

The microfinance enterprise mannequin was born within the marginalized neighborhoods of main cities, however these establishments are actually current in most mid-sized cities the place additionally they cater to the wants of surrounding rural communities. Rates of interest, which vary from twenty to eighty per cent, replicate the chance of default related to their clientele and the excessive transaction prices related to administering tens of 1000’s of small loans [xiii] Most microfinance entities function with capital obtained from standard banks and funding funds and pay these establishments commonplace business rates of interest (5 to eight per cent). Microfinance, which is marketed as a pro-poor public service, can be a extremely profitable enterprise mannequin. [xiv]

Presumably, a farmer can be a low-risk debtor when in comparison with a person engaged in speculative commerce, however the monetary sector considers small household farms as high-risk collectors as a consequence of climate and pests. In Peru, inflation-adjusted rates of interest for small farmers are between twenty and thirty per cent, a price that’s out of attain for all agricultural manufacturing programs, a lot much less smallholders residing on the sting of poverty. Giant- and medium-scale producers have entry to standard types of credit score as a result of they’ll meet the circumstances required by lending businesses, significantly authorized title to their land and a documented historical past of manufacturing and gross sales. Even these numbers are disappointing, nonetheless. In 2019, authorities businesses reported that $33 million had been loaned to 4,199 beneficiaries in a rustic with an estimated 2.2 million farmers. [xv]

Peru has tried varied fashions to channel funds by way of financial savings and mortgage cooperatives (COOPACS), privately-owned rural financial savings banks (Caja Rurales), blended associations of personal capital and native authorities (Caja Munciaples) and a specialised state-owned improvement financial institution (Agrobank). None have succeeded in offering inexpensive credit score to small farmers. The newest try, a particular fund (FAE-Agro) that’s capitalized by the nationwide improvement financial institution (COFIDES) is doomed to failure as a result of recipients are required to point out authorized title for his or her properties, a situation loved by solely fifteen per cent of the small farmers of Peru (see Chapter 4). [xvi]

Civil society has had higher success working with grower’s associations that concurrently present technical assist in agronomics, pest administration and enterprise administration for particular person growers and their umbrella organizations. Profitable initiatives are characterised by a long-term dedication on the a part of civil society organizations and specialty consumers keen to put money into applications that assure a provide of espresso and cacao that’s licensed as deforestation-free, natural, indigenous and/or gender optimistic.

Bolivia’s agricultural sector is just like Brazil’s but in addition fairly totally different. There’s a restricted variety of large-scale producers, fairly just a few (higher) middle-class landowners and a big, dynamic small-farm constituency. It lacks, nonetheless, a state sponsored rural credit score program that obligates the monetary business to channel cash to its producers. Giant and mid-scale farmers entry capital by way of the commodity buying and selling corporations, in addition to from an off-the-cuff credit score market finest described as a normalized system of mortgage sharks. Ranchers depend on household capital, private financial savings or money circulate generated by city enterprise ventures (medical providers, actual property, commerce).

The smallholders of Bolivia are additionally lively individuals within the nationwide foodstuffs market, and fairly just a few have developed into profitable soybean farmers. Many are descendants of Andean indigenous migrants with a robust cultural custom of financial savings and funding, traits shared by a big Mennonite group. These teams even have an off-the-cuff credit score market they use for short-term finance. Microfinance establishments are current and, as in Peru, they’ve opened places of work in regional cities. Authorities insurance policies to distribute money earnings to aged and school-age youngsters have motivated lots of of 1000’s of rural households to open financial savings accounts. Excessive rates of interest, nonetheless, preclude their means to borrow cash to put money into agricultural expertise.

Ecuador’s microfinance business is dominated by financial savings and mortgage associations that serve each city and rural populations; rates of interest vary between 25 and 28 per cent. The normal banking system treats agricultural credit score as one in every of a number of sorts of ‘productive enterprise’, all of which have annual rates of interest between eight and twelve per cent. [xvii] The federal government hopes to assist its agricultural sector by way of a newly constituted public financial institution, BanEcuador, which presents loans particularly designed for, and marketed to, producers of espresso, cacao and oil palm. Producers can borrow as much as $150,000 for each short-term credit score and to enhance productive capability (plantations); for the latter, phrases of as much as fifteen years can be found, with a grace interval of between three to 5 years. [xviii] Loans better than $20,000 require a mortgage assure.

The BanEcuador applications present an understanding of the wants of their potential clientele, together with cost schedules based mostly on the money circulate of particular person manufacturing methods (month-to-month, quarterly, or yearly). Annual rates of interest vary between 9.75 and 16.5 per cent, consistent with enterprise loans from non-public banks and considerably decrease than these out there from microfinance establishments. Regardless, rates of interest at this degree aren’t prone to catalyze a wave of much-needed funding in agricultural manufacturing. In 2019, BanEcuador loaned $3 million to 700 producers, a comparatively small quantity that will translate into solely about 500 hectares of recent oil palm plantations.

Colombia has a program just like the SNCR of Brazil. It’s administered by FINAGRO (Fondo Para el Financiamiento del Sector Agropecuario), a public company that operates as a second-tier lender to personal establishments and a guarantor for quite a lot of monetary merchandise, together with quick and long-term credit score and crop insurance coverage. The FINAGRO system establishes commonplace phrases and charges for a diversified portfolio of credit score merchandise particularly designed for the wants of producers in agriculture, livestock and plantation forestry. Packages span the landholder spectrum and embody particular initiatives for producer associations. Rates of interest vary from three to 10 per cent above a base price set by the central financial institution, which has fluctuated between three and 5 per cent since 2010 . FINAGRO additionally presents reductions to the middleman establishment to make the mortgage extra accessible to the retail shopper. [xix] For a fee, FINAGRO will assure the mortgage for the producer, which is basically a type of crop insurance coverage; it additionally presents standard crop insurance coverage to guard the producer and the lending company from local weather danger and pests.

On the nationwide scale, FINAGRO facilitated monetary credit score value roughly $7.1 billion in 2020, up from $2.9 billion in 2011, rising by a formidable twenty per cent yearly over the identical interval. Though the Colombian program is properly designed and considers each market actuality and the particular wants of producers, it operates solely on landscapes the place the state has imposed the rule of legislation. Sadly, Amazonian landscapes are characterised by the absence of the state, both as a result of they’re distant or as a result of they’re underneath the management of armed criminals. In Amazonian departments, FINAGRO facilitated solely about $80 million in 2020, a quantity that has remained basically flat since 2010. [xx] Roughly half of that was in Caquetá and, presumably, was lent to the cattle sector, which can be the most important single recipient of agricultural credit score throughout the FINAGRO system.

Harnessing Finance to Change Conduct

Rural finance has monumental potential to reform standard agricultural manufacturing programs. Consequently, it’s a widespread element of coverage proposals to fight deforestation the place it’s considered as a ‘carrot’ to accompany the ‘sticks’ that search to coerce landholders to reform land use practices (see Chapter 7).

The expertise of the Cattle Settlement and the Soy Moratorium present the potential when business intermediaries are used as stress factors to remove unlawful deforestation. These initiatives, which deal with excluding transgressors from provide chains, may very well be expanded by conditioning entry to the billions of {dollars} of short-term loans offered yearly by worldwide commodity merchants and meat packing corporations. As a driver of sustainability, credit score is perhaps much more efficient if these identical corporations supplied long-term loans with concessionary charges that motivated their suppliers to revive forest that had been transformed illegally within the current previous.

Comparable adjustments to the Sistem Nacional de Credito Rural (SNRC) may likewise catalyze widespread change, significantly throughout the Brazilian cattle business the place many years of over grazing have degraded tens of millions of hectares of pasture. Pasture restoration begins and ends with soil conservation, which depends on administration practices to extend soil natural matter and, within the course of, create a long-term carbon sink (see Chapter 4). That is basically the purpose of Brazil’s Agricultura de Baixo Carbono (ABC) program, a subcomponent of the SNCR with enticing rates of interest and an prolonged pay-back interval. [xxi] Supported applied sciences embody diminished tillage, pasture renovation, built-in crop and livestock administration, and the restoration of riparian habitat (see Chapters 4 and Chapter 6). The ABC program has loved modest success – in 2020, this system lent roughly $R 2 billion ($400 million) – nonetheless, that’s lower than one per cent of the whole channeled by means of the SNCR in 2020. The potential, given Brazil’s historical past of utilizing the SNCR to subsidize its agricultural producers, is very large and eminently sensible.

Inexperienced bonds and related sorts of ESG finance are the quickest rising element of Brazil’s monetary sector. Worldwide capital markets are frenetically searching for viable tasks to fulfill large international demand for ESG funding. Brazil’s potential to fulfill this demand by decreasing GHG emissions attributable to deforestation might be leveraged by an equally large capability to sequester carbon by way of economically advantageous applied sciences to make standard agriculture extra sustainable. This kind of risk-limited inexperienced funding might be a magnet for international buyers. The nation’s attractiveness is bolstered by the nation’s cultural dedication to a market economic system, its openness to worldwide capital and the plentiful pure sources which are the inspiration of its rural economic system.

The efficiency of inexperienced bonds in Brazil is being intently watched by coverage analysts, due to their potential to drive local weather change motion ‘at scale’. Nonetheless, these devices, and others like them, danger being labeled as ‘greenwash’ in the event that they achieve enhancing the efficiency of collaborating corporations however fail to resolve the deforestation disaster. That consequence will rely, largely, on the flexibility of the Brazilian state – and its non-public sector companions – to include smallholders in a revitalized and reformed rural economic system. Brazil has created the institutional mechanisms for pursuing that purpose (INCRA, EMBRAPA, PRONAF, SNCR), however its observe file for dealing equitably with its personal residents is just not significantly encouraging.

Within the Andes Amazon, the potential to hyperlink finance, together with quick and long-term credit score, with efficient insurance policies to rework their agricultural sector is much more difficult. No nation has succeeded in delivering inexpensive credit score to their Amazonian populations, nor develop an extension system able to guaranteeing these sources are invested in productive enterprises which are globally aggressive and environmentally sustainable. If they’ve any benefit, in comparison with Brazil, it’s the preponderance of smallholder programs that creates a precondition that favours social fairness. That benefit, nonetheless, is a double-edged sword. It might be sure that a reformed system might be socially sustainable, but it surely additionally makes it enormously harder to implement.

If the Amazon forest is to be saved, deforestation should finish. Full cease. World and nationwide markets, nonetheless, will proceed to demand extra commodities from the farmers and ranchers of the Southern Amazon and Andean Piedmont. They are going to reply by rising manufacturing. Full cease. They may intensify their programs by investing in expertise, or they may buy extra land to develop manufacturing. Left to their very own units, they’d pursue each choices as a result of that’s the logical pathway to maximise the return on their investments. Farmers and ranchers don’t function in a vacuum, nonetheless. Producers, massive and small, allocate their sources in response to regulatory and market forces that govern the agricultural economic system. Among the many most necessary are the constraints and incentives in rural actual property markets (see Chapter 4). When the forest frontier ceases to be a supply of cheap land, the agricultural sector might be compelled to put money into the land underneath manufacturing — and solely the land underneath manufacturing. Making that occur sooner, quite than later, is crucial for saving the Amazon.

[i] MAPA – Ministério da Agricultura, Pecuária e Abastecimento. 2020. Política Agrícola, Plano Safra 2020/2021 entra em vigor nesta quarta-feira Plano Dafra: https://www.gov.br/agricultura/pt-br/assuntos/noticias/plano-safra-2020-2021-entra-em-vigor-nesta-quarta-feira

[ii] Ibid.

[iii] Strassburg, B.B., T. Brooks, R. Feltran-Barbieri, A. Iribarrem, R. Crouzeilles, R. Loyola… and A. Balmford. 2017. ‘Second of fact for the Cerrado hotspot’. Nature Ecology & Evolution 1 (4): 1–3.

[iv] Yuri Ramos, S. and G. Bueno Martha Jr. 2010. Evoluçcão da Politica de Créditop Rural Brasileria, EMBRAPA Cerrado, Brasilia.

[v] Souza, P., S. Herschmann and J. Assunção. 2020. Política de Crédito Rural no Brasil: Agropecuária, Proteção Ambiental e Desenvolvimento Econômico. Local weather Coverage Initiative, Rio de Janeiro: https://www.climatepolicyinitiative.org/pt-br/publication/politica-de-credito-rural-no-brasil-agropecuaria-protecao-ambiental-e-desenvolvimento-economico/

[vi] Forests & Finance Coalition. 2021. Finance knowledge, Discover the information: https://forestsandfinance.org/knowledge/

[vii] IMEA – Instituto Mato-Grossense de Economia Agropecuária. 2021. CUSTO DE PRODUÇÃO, DSoja GMO: https://www.imea.com.br/imea-site/relatorios-mercado-detalhe?c=4&s=3

[viii] Forests & Finance Coalition, Finance knowledge.

[ix] OXFAM – BRASIL. 2016. Terrenos da Desigualdade: https://www. oxfam. org. br/publicacoes/terrenos-da-desigualdade-terra-agricultura-e-desigualdade-no-brasil-rural

[x] Local weather Bond Initiatives. 2021. https://www.climatebonds.web/recordsdata/reviews/cbi-brazil-agri-sotm-eng.pdf

[xi] FAIRR Farm Animal Funding Danger and Return Initiative (2019) https://www.fairr.org/article/marfrigs-transition-bond

[xii] Pinzon, A. 2019. Redefining finance for agriculture: Inexperienced agricultural credit score for smallholders in Peru. World Cover: https://www.meda.org/innovate/innovate-resources/822-partner-publication-redefining-finance-for-agriculture-green-agricultural-credit-for-smallholders-in-peru-eng/file/

[xiii] SBS – Superintendencia de Banca, Seguros y AFP. 2021. Tasa de interés promedio del sistema de cajas rurales de ahorro y crédito: https://www.sbs.gob.pe/app/pp/EstadisticasSAEEPortal/Paginas/TIActivaTipoCreditoEmpresa.aspx?tip=C

[xiv] Sengupta, R. and C.P. Aubuchon. 2008. ‘The microfinance revolution: An summary’. Federal Reserve Financial institution of St. Louis Evaluation 90 (Jan./Feb.)

[xv] Gestión. 26 Nov. 2020. El FAE-AGRO Es Un Completo Fracaso, Grupo Propuesta Ciudadana: https://gestion.pe/weblog/propuesta-ciudadana/2020/11/el-fae-agro-es-un-completo-fracaso.html/?ref=gesr

[xvi] Ibid.

[xvii] ASOBANCO – Asociación de Bancos del Ecuador. 2019. Informe Técnico: Tasas de Interés, Volumen N°1: https://www.asobanca.org.ec/file/2286/obtain?token=IHmybA6t

[xviii] BanEcuador. 29 Might 2021. Credito Productivo Palma, Microempresas: https://www.banecuador.fin.ec/productos-ciudadanos/credito-micro/productos-microempresas/credito-palma/

[xix] FINAGRO – Fondo para el Financiamiento del Sector Agropecuario. 2 June 2021. Productos y Servicios, Portfolio de Servicios: https://www.finagro.com.co/productos-y-servicios

[xx] FINAGRO – Fondo para el Financiamiento del Sector Agropecuario. 2 June 2021. Estadísticas: https://www.finagro.com.co/estadpercentC3percentADsticas

[xxi] Banco do Brasil (26 July 2021) Agricultura de Baixo Carbono (ABC), https://www.bb.com.br/pbb/pagina-inicial/agronegocios/agronegocio—produtos-e-servicos/credito/investir-em-sua-atividade/agricultura-de-baixo-carbono-(abc)

[ad_2]

Source link

{kind=link}