[ad_1]

That’s the headquarters of the Individuals’s Financial institution of China which, in distinction with the U.S. Federal Reserve, has shifted to stimulus mode to defend the world’s largest development engine from the Evergrande property stoop, virus lockdowns and better world borrowing prices because the Fed tightens.

Tasked with staving off destabilizing unemployment and a debt implosion, Governor Yi Gang’s PBOC has a newfound autonomy unthinkable a decade in the past which will show essential in retaining China’s growth buzzing above 5% this yr.

It’s summed up in a brand new mantra heard from China’s financial coverage makers, roughly translated: “We set our personal agenda.”

A long time of stop-start reform have led to freer forex actions and extra refined capital controls, that means that even because the Fed speeds towards a primary fee hike since 2018, China’s central financial institution has autonomy to maneuver within the different route.

And having prevented the all-out stimulus of Western friends when the Coronavirus first struck in early 2020, the PBOC finds itself with dormant shopper costs and room to “open the financial coverage tool-box.”

For China, that units the stage for a triple dose of help from elevated lending, decrease borrowing prices and — probably — a weaker yuan that may enhance exports. The PBOC has already made a down cost on fee cuts and most economists count on extra to return.

By China’s regular requirements, the prize for profitable stimulus will probably be small — extra stopping a continued slide in development than driving a contemporary acceleration. And previous coverage errors — permitting a debt bubble to increase to huge dimension — add threat to the outlook and a constraint on the PBOC’s freedom of maneuver.

If Yi and his group can pull it off, although, the enhance from PBOC stimulus ought to offset not less than among the drag on world development from Fed tightening. Worldwide Financial Fund projections present China is ready to contribute greater than one-quarter of the whole enhance in world gross home product within the 5 years by way of 2026, exceeding the U.S.’s roughly 19% share.

These with most publicity to China’s financial system — commodity exporters like Australia and Asian neighbors like South Korea — will breathe the largest sigh of reduction if efforts at stabilization succeed. Nations with weaker ties to China however extra publicity to dangers because the Fed tightens — like Mexico and Turkey — have much less to achieve.

Many buyers are betting on a rebound in Chinese language belongings after the MSCI China Index of shares lagged the S&P 500 by 49 proportion factors final yr, the largest hole since 1998. Strategists at Goldman Sachs Group Inc., BlackRock Inc. and HSBC Holdings Plc are amongst these to have turned bullish on the nation’s shares.

Diverging PBOC and Fed insurance policies replicate diverging trajectories for the Chinese language and U.S. economies.

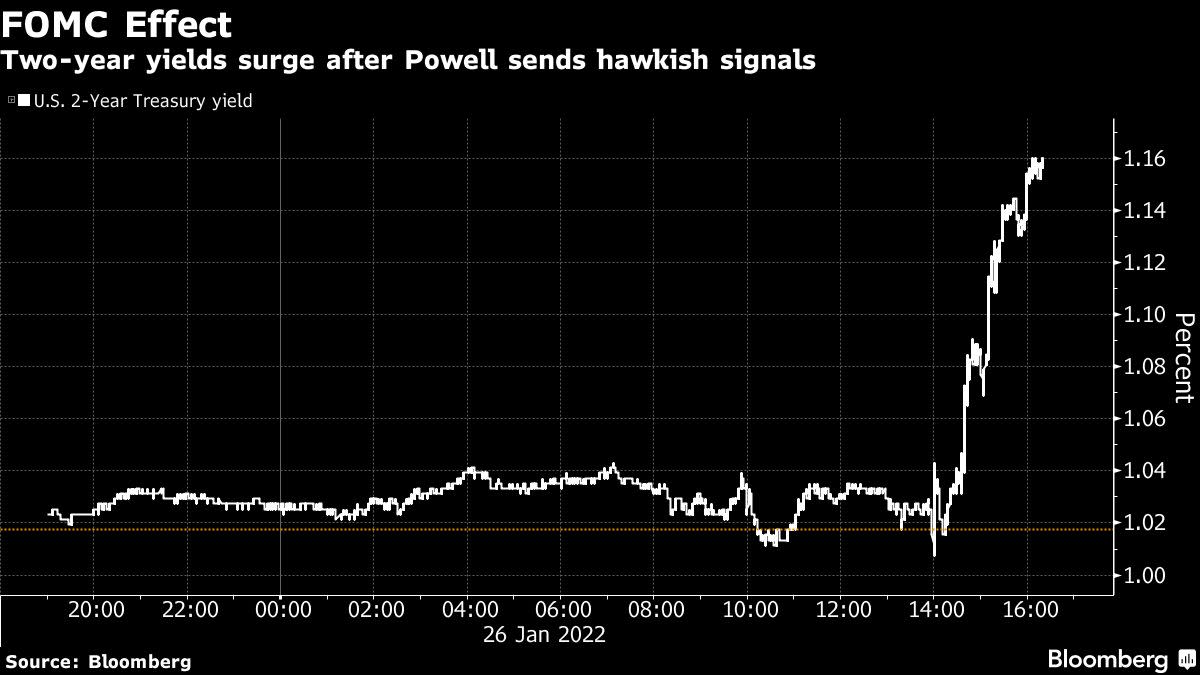

Within the U.S., the mix of excessive vitality and meals costs, provide shortages, and rising rents has pushed the patron worth index to 7% yr on yr. Markets now view a primary Fed fee hike in March as near a certainty, with the hawkish tone from Chair Jerome Powell on the January FOMC press convention confirming the view. Bloomberg Economics forecasts 4 extra over the course of the yr, in addition to a speedy begin to working belongings off the bloated steadiness sheet.

The PBOC is shifting in the other way. Its 10-basis level reduce in borrowing prices final week and a pledge to make use of extra instruments was a transparent sign that the precedence has shifted away from reining in monetary dangers and towards supporting development.

The most important drag comes from the sector that was as soon as China’s most dependable development driver — actual property. A default by large developer Evergrande has shaken market confidence, tightening financing circumstances. Gross sales and new building at the moment are falling at a speedy clip. With property contributing — instantly and not directly — about one in each 4 yuan of GDP, that’s set to weigh on all the things from demand for iron ore to spending on dwelling electronics.

Then there’s the virus. With the Xi’an outbreak triggering extra Covid-19 circumstances than any for the reason that preliminary wave at first of 2020, and the arrival of world athletes for the Winter Olympics including to the petri dish, there’s the danger of additional lockdowns. Because the expertise of the outbreak in summer time 2021 demonstrated, even short-lived and focused measures to manage the unfold of the virus can take a extreme toll on shopper spending.

Pull these items collectively, and China once more faces the danger of a major blow to development.

A repeat of the huge contraction in output seen at first of 2020 appears unlikely. Nonetheless, the mixed impression of nationwide property stoop and native lockdowns may very well be extreme. In its latest Monetary Stability report, the PBOC envisioned a worst case the place development drops near 2% — approach beneath the consensus forecast of 5.2% for 2022 and beneath even essentially the most pessimistic forecast in Bloomberg’s survey of economists.

For the central financial institution, the very best likelihood of steering a path away from such dire eventualities lies in harvesting the fruits of previous reforms.

It’s an concept from the academy that — from former Governor Zhou Xiaochuan to his successor Yi — has held a permanent fascination for high PBOC officers: the unimaginable trilemma. That’s the idea that an financial system can’t management its trade fee, open to cross-border capital flows and set its personal rates of interest on the similar time — it should choose two of the three.

China’s expertise illustrates why.

In 2002, when Zhou took over on the helm of the central financial institution, China’s yuan was pegged to the greenback. The capital account was closed in concept, however in apply it was simple to dodge controls and transfer funds in and overseas.

In consequence, the PBOC discovered itself on the horns of the trilemma, with restricted financial coverage independence. Set rates of interest too excessive relative to the Fed, and there can be large capital inflows. Too low, and capital would circulation out.

With the yuan undervalued, rates of interest confined inside a slender vary, and crude credit score quotas the primary instrument for managing the ups and downs, the financial system ran scorching and asset costs soared. The seeds of later issues — just like the Evergrande property bubble — had been sown.

The transfer in the direction of extra market-driven trade charges started in 2005 with a one off 2% appreciation towards the greenback. The street forward was removed from clean. Sluggish progress was a relentless supply of irritation for the U.S. — which noticed an undervalued yuan as an unfair supply of aggressive benefit for China’s exporters. Some reform steps misfired — as when a mini yuan devaluation in 2015 triggered a world market panic.

Even so, within the years that adopted — with stops, begins and main missteps alongside the way in which — the PBOC moved the yuan towards truthful worth, and all-but eradicated day-to-day intervention out there. That painstaking course of has shifted China to a brand new regime with a near market set trade fee, focused capital controls, and financial coverage that’s now extra autonomous from outdoors affect.

“As a result of China’s trade fee coverage has turn out to be extra versatile, sustaining financial coverage independence has turn out to be a lot simpler,” says Yu Yongding, a former PBOC adviser and long-time champion of yuan liberalization. His outdated colleagues agree. Of their Financial Coverage report on the finish of 2021, the PBOC cities yuan flexibility as one of many large causes for resilience because the Fed tightens.

A refined set of capital controls additionally play a task. Whilst China permits extra two-way motion in its forex and extra world buyers in to snap up its belongings, strict controls stay on people’ and corporations’ skill to maneuver cash overseas. A shift in financial knowledge within the West during the last decade has seen the IMF endorse capital controls it had as soon as known as for nations to abolish.

For China, the advantages of reforms can’t arrive quickly sufficient. Decrease borrowing prices and ample liquidity will assist forestall contagion from the Evergrande default spreading too far. They need to additionally stoke funding — offsetting not less than among the drag as property building slumps.

Up to now, if decrease charges drove yuan weak spot that may be a panic sign, requiring the PBOC to wade in to stabilize the market. Now, with acceptance that the yuan is a two-way wager, forex weak spot can be a further profit by serving to drive export earnings.

For the remainder of the world, the looming risk of accelerated Fed tightening is a stumbling block on the trail to restoration. By no means one to overlook a chance to current China as a pressure for stability, President Xi Jinping used his speech to the Davos discussion board this month to warn of “ critical damaging spillovers” when the Fed slams on the brakes.

The issue is particularly extreme for China’s fellow rising markets, which face the prospect of capital outflows as U.S. charges rise. The prospect of PBOC stimulus stoking Chinese language demand guarantees not less than a partial offset, particularly for nations like Chile and Brazil that rely China amongst their largest export prospects.

For Asia’s central banks and monetary markets, divergence between the Fed and the PBOC will — over time — introduce a brand new dynamic to navigate. As China’s monetary system opens wider, PBOC coverage will begin to train an affect on Asia’s markets that collides with that of the Fed. From Seoul to Jakarta, central bankers and FX merchants must determine whether or not it’s U.S. or China coverage that’s the stronger anchor. Already, some regional currencies are monitoring the yuan greater than they used to.

Success at stabilizing the financial system is much from assured. The PBOC’s progress on reforms got here too late to stop an explosion in debt, which now stands at near 285% of GDP. The results of which might be evident within the Evergrande debacle, and the necessity to deflate the bubble constrains capability for stimulus.

In a worst-case situation for the virus — with widespread contagion triggering a brand new nationwide lockdown — no quantity of fee cuts or yuan depreciation would forestall a plummet in output.

Nonetheless, at a essential second, the PBOC’s patiently pursued reforms have purchased them not less than a bit more room for stimulus. Will or not it’s sufficient? China’s leaders, rising markets warily eyeing Fed tightening, and buyers centered on the danger of debt disaster, hope the reply is sure.

[ad_2]

Source link

{kind=link}