[ad_1]

Welcome to my new weekly fintech-focused column. It’s an unbelievable time to be a monetary expertise journalist. In addition to the truth that over 20% of all enterprise {dollars} final yr went into fintech startups, I’m notably excited concerning the many ways in which this expertise helps increase inclusion all around the world. Whereas this pandemic has sucked on 100 totally different ranges, one good factor to have come out of it’s that customers and companies have pressured extra fintech to exist, and that’s factor.

I’ll be publishing this each Sunday, so in between posts, make sure to take heed to the Fairness podcast and listen to Alex Wilhelm, Natasha Mascarenhas and I riff on all issues startups!

There was loads of drama at on-line mortgage lender Higher.com during the last couple of months and it seems that simply because its notorious CEO Vishal Garg is again on the helm, there’s nonetheless no scarcity of controversy surrounding the corporate. Earlier this week, Axios’ Dan Primack revealed that investor SoftBank, “in its obvious zeal to again the corporate,” promised to offer Garg the 1.9% voting rights tied to its authentic funding, “contingent on the ultimate settlement of sure authorized proceedings (which has not but occurred).” For individuals who haven’t been following this saga, Garg has acquired a ton of adverse press for his unfeeling means of shedding 900 folks over Zoom, berating his personal buyers over electronic mail and accusing workers of being “lazy” and “dumb dolphins.”

We’ve all been questioning how this man can nonetheless be operating the present and maybe SoftBank’s situations assist clarify it. In the meantime, one former staffer tells me that Higher workers are so upset that Garg is again, that they’re leaving the corporate in droves. Reportedly, workers at each degree – from mortgage officers to senior executives (a few of whom are believed to be leaving probably hundreds of thousands of {dollars} in fairness on the desk). As the worker instructed me, “It’s an astonishing fall from grace. It will not be a stretch to say that the highest expertise and a whole lot from each division have fled within the wake of Zoomgate.”

Picture Credit: Higher.com CEO Vishal Garg / LinkedIn

However that’s not all. Now that Garg is again, he’s apparently paranoid about issues being leaked to the media and in line with one worker, he and the remainder of the execs nonetheless there “have put every part on lockdown.”

For instance, engineering managers have been mentioned to have had an AMA (Ask Me Something) with Garg and solely in-person staff have been allowed to attend. These workers needed to signal NDAs and place telephones in paper baggage, and there have been even steel detectors to verify nobody had recording units. Additionally, the corporate has reportedly disabled sharing of Google paperwork internally they usually’ve blocked entry to all companywide dashboards – doubtless as a result of enterprise has in all probability suffered dramatically. As the worker put it: “There’s no transparency into something. Vishal doesn’t belief anybody.”

Now let’s discuss funds

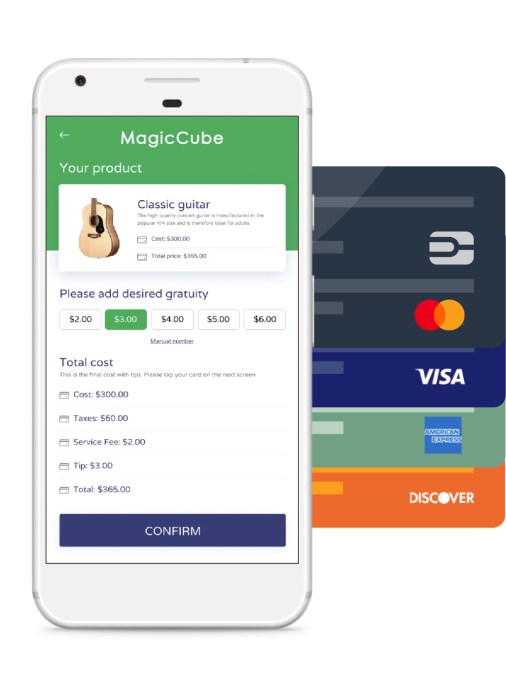

Small companies would possibly quickly be capable to settle for funds utilizing their iPhones with out the necessity for additional {hardware}, in line with this piece, which cites Bloomberg. That is fascinating as a result of if true, Apple could possibly be seen as taking up Sq. within the contactless funds house. I discovered all this notably intriguing as a result of in October, I wrote a couple of startup named MagicCube – which is backed by the likes of Visa – that’s constructing expertise that may influence Android customers.

Picture Credit: MagicCube

That firm’s software-based tech provides retailers a technique to settle for card funds on any client system with no reader or additional {hardware} required. CEO and co-founder Sam Shawki instructed me in October that he believed his startup “would be the dominant social gathering on the Android aspect, which is 85% of the universe.”

Final week, Shawki instructed me he has a good larger imaginative and prescient relating to contactless funds:

Apple’s entry into the funds’ acceptance market will ignite the house for certain. However there’s a good higher imaginative and prescient of softPOS acceptance that goes past Apple’s: one that’s constructed on an open platform, the place all units and all card networks are welcome, cost knowledge is really secured to the best requirements, and platforms are simply scalable. A broad ecosystem of expertise pioneers, funds networks, issuers, and acquirers are creating a softPOS resolution that extends past any firm’s walled backyard.

On this imaginative and prescient, retailers personal their very own knowledge. On any system and working system, softPOS is simple to implement, and requires no certifications. Costly, devoted units turn into out of date.. As these applied sciences proliferate in on a regular basis life, we’ll witness the arrival of the Web of Funds…Collectively, prior to you would possibly assume, the newcomers will unseat the incumbents. The meteor is about to hit. And we’ll all be higher off for it.

The truth that extra corporations are making it simpler to pay with out contact isn’t a surprise and welcome as that spells safety and comfort for customers. Will probably be thrilling to look at how this all performs out.

Notable rounds and a brand new fund

Our Nigeria-based startups reporter, Tage Kene-Okafore final week wrote about Esusu, a New York-based fintech firm that targets immigrant and minority teams and supplies hire reporting and knowledge options for credit score constructing, that raised $130 million in a Sequence B spherical led by SoftBank Imaginative and prescient Fund 2. The funding gave four-year-old Esusu a valuation of $1 billion, making it one of many only a few black-owned unicorns within the U.S. and globally (like to see this checklist rising!). Esusu co-founders and co-CEOs Nigerian-born American Abbey Wemimo and Indian American Samir Goel come from immigrant houses and say they skilled firsthand monetary exclusion. That led them to start out Esusu in 2018 in an effort to construct the credit score scores of immigrants and African-People and “leverage knowledge to bridge the racial wealth hole” by way of rental funds.

Esusu

Tage additionally lined NALA, a Tanzanian cross-border funds firm that just lately pivoted from native to worldwide cash transfers, and its latest $10 million seed elevate. The startup’s mission is to construct the “Revolut for Africa.” You may learn all about it right here.

In addition to Esusu, final week noticed one more fintech unicorn being born. CaptivateIQ, which claims to automate fee workflows utilizing AI, raised its third spherical in 20 months. Lower than 10 months after elevating its $46 million Sequence B, CaptivateIQ raised $100 million in a Sequence C spherical at a $1.25 billion valuation. The San Francisco-based startup, which has developed a no-code SaaS platform to assist corporations design personalized gross sales fee plans, says it “greater than tripled” its income in comparison with the yr prior, though it declined to supply exhausting income figures. A trio of companies co-led CaptivateIQ’s newest funding, together with ICONIQ Development and present backers Sequoia and Accel.

In M&A exercise, funding banking agency UBS picked up monetary robot-advisor Wealthfront for $1.4 billion in an all-cash deal. Alex unpacked the deal for us right here.

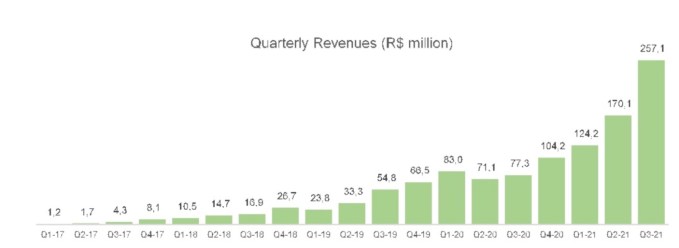

Unsurprisingly, Latin America continues to be a hotbed of fintech exercise. I lined Brazilian lender Creditas’s $260 million Sequence F funding that valued the corporate at $4.8 billion. That’s up from the fintech’s $1.75 billion valuation on the time of its $255 million elevate in December 2020. Constancy Administration led the newest spherical. Some of the fascinating issues about this firm, moreover all of the cool companies it supplies (together with providing Latin People a technique to borrow cash at a MUCH decrease rate of interest than conventional banks provide) is share all its financials! Severely, the extent at which this firm shares the main points of its funds is one thing to be admired and we want all startups would observe swimsuit.

Picture Credit: Creditas

Impressively, within the third quarter of 2021, Creditas says it notched US$46.8 million in income – up 233% from $14 million within the 2020 third quarter. It has been targeted on progress, so it’s nonetheless reporting a loss. However founder and CEO Sergio Furio instructed me that he tasks annualized income of about $200 million for 2021. Not unhealthy in any respect! I’m excited to look at this one continue to grow.

I additionally lined a brand new fintech fund began by a real fintech influencer and all-around good individual, Nik Milanović. For over two years, Nik has been placing out a e-newsletter referred to as This Week In Fintech, working at Google Pay and angel investing. Most significantly, he’s been constructing a real neighborhood of fintech lovers all around the globe. Now he’s placing his cash the place his mouth is and launching his personal enterprise fund, referred to as merely The Fintech Fund. Nik is making an attempt to lift $10 million for his fund, which has a bunch of cool LPs together with buyers who put cash in fintech startups by different autos (corresponding to Bain Capital, Higher Tomorrow Ventures and Cowboy Ventures’ Jillian Williams) and a a number of founders together with NerdWallet co-founder Jake Gibson and The Block’s Mike Dudas. Additionally, I like the truth that the fund has an express goal of over 25% or extra of its {dollars} and whole variety of investments going to founders from underrepresented backgrounds. I discussed inclusion up high and it’s value noting that Nik is large on it too. GO NIK!

Picture Credit: Founder Nik Milanovic / The Fintech Fund

That’s it for now. I hope you had as a lot enjoyable studying this as I did writing it. Now, go get pleasure from what’s left of this weekend!

[ad_2]

Source link

{kind=link}